Environmental, social and governance (ESG) topics have received considerable attention over the past years, being largely driven by investors seeking to understand the risks and opportunities that could impact financial performance. In addition, stakeholders including customers and employees are holding companies up to higher standards, using ESG data to evaluate a company’s performance on topics they personally find important. This can include the diversity of the workforce or the company’s efforts in reducing its environmental footprint. In the absence of regulation and a growing market demand for transparency in sustainability-related data, an overflow of voluntary ESG reporting standards and frameworks have emerged. Currently hundreds of these frameworks and standards exist creating a lot of noise and confusion for the individuals that have to navigate this landscape. Therefore, we aim to provide some clarity the different ESG standards and frameworks that currently exist and how this landscape is changing.

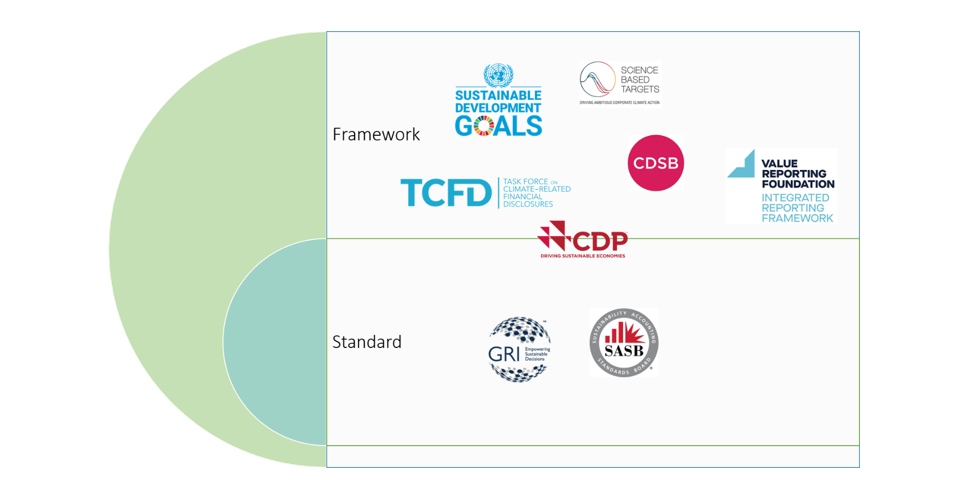

It is important to first know the difference between a standard and a framework. A framework such as the Sustainable Development Goals (SDGs) provide a reference for companies on sustainability but leave room for interpretation in the direction a company may want to go. Thus, frameworks do not provide any metrics or reporting obligations. A standard like the Global Reporting Initiative (GRI) makes a framework actionable and contains detailed information including specific criteria and metrics which outline exactly what a company should report on for each topic. The figure below gives an overview on of the most common frameworks and standards.

Key ESG Frameworks

The Sustainable Development Goals

The Sustainable Development Goals (SDGs) framework, launched by the United Nations in 2015 are a series of 17 goals to be achieved by 2030. Each goal focuses on one global challenge, ranging from poverty, inequality and zero hunger to clean energy, and climate change. Many of these challenges can be addressed by the private sector and thus the SDGs act as a guide for companies on how to do business responsibly. Companies typically align their operations with the SDGs by choosing the targets and goals they believe will have the largest impact in terms of risk and opportunity on their business in the short, medium and long term. The SDGs are commonly also used to understand material topics, develop sustainability strategies, communicate and report on goals and activities.

Task Force for Climate-Related Financial Disclosures

The Task Force on Climate-Related Financial Disclosures (TCFD) is a framework developed to help companies specifically disclose on climate-related risks and opportunities. For example, the TCFD asks companies to understand how physical climate risks such as droughts or transitional risks such as carbon taxes may financially impact their business. Companies should also be aware of opportunities as the development of sustainable products can give them access to new markets and revenue streams. As a framework, the TCFD provides recommendations for disclosure rather than prescriptive guidelines which are centered around four main areas including governance, strategy, risk management, metrics and targets. Key is that companies start to understand the financial implications of climate change.

Integrated Reporting Framework

The Integrated Reporting (IR) Framework was established in 2010 by the International Integrated Reporting Council (IIRC) with the aim of developing a globally accepted framework of principles that would govern and provide information on what should be included in the content of an integrated report. An integrated report brings together material information on a company’s strategy, and governance but also reflects the commercial, social and environmental context in which a company operates. Traditional reporting leaves out the social and environmental contexts.

In the summer of 2021, the IIRC merged with the Sustainability Accounting Standards Board (SASB) to form the Value Reporting Foundation. The two are complementary as the IR describes all relevant value creation topics and how to integrate them in a corporate report whereas SASB provides the definitions and data that should be reported on for each industry. The merger ensures a holistic way for companies to communicate about their organization and sustainability.

Science Based Targets Initiative

The Science based targets initiative (SBTi) is another framework that is gaining momentum. In 2018, the Intergovernmental Panel on Climate Change (IPCC) issued a warning that global warming should not exceed 1.5⁰C to avoid the most catastrophic impacts of climate change. As a result, the SBTi was born to guide companies in setting net-zero emission targets that are in line with a 1.5⁰C scenario future. Essentially the SBTi verifies that the emission reduction targets that a company sets are effective and positively contribute to transitioning to a zero-carbon society no later than 2050.

The Climate Disclosure Standards Board (CDSB)

Similar to the integrated reporting framework, the CDSB was founded in 2007 and developed a framework aimed to help companies disclose on ESG data that is financially material to their organization and to their investors.

Key ESG Standards

Global Reporting Initiative (GRI)

The Global Reporting Initiative (GRI) is one of the most widely used reporting standard in the world, and focuses on a company’s economic, environmental, social and governance performance. The Initiative was founded in 1997 in response to the Exxon Valdez oil spill which spurred public outcry on the lack of transparency on the environmental impact made by Exxon. The GRI hold companies accountable and ensure they adhere to a responsible environmental conduct. While originally focused solely on the environment, the standard was later broadened to also include social, economic and governance issues such as health and safety and human rights. The GRI reporting standards are composed of three sections: The GRI universal standards, the GRI sector standards and the GRI Topic standards. Each standard contains relevant disclosure metrics that provide companies with a structured guidance what and how they should report. This has increased company accountability and transparently on their sustainability progress to all stakeholders including investors.

Sustainability Accounting Standards Board (SASB)

Founded in 2011, the Sustainability Accounting Standards Board (SASB) aims to help companies disclose financially material sustainability information to their investors. The SASB standard is very similar to GRI also focusing on ESG topics but instead considers the financial impacts of sustainability. The main difference between SASB and GRI are the stakeholders, while GRI is for all stakeholders SASB predominantly evolved by focusing on the disclosure of financially material ESG topics that are expected to impact an organization. Consisting of 77 industry specific disclosure standards that outline financially material topics for each industry, SASB helps organizations classify, assess and communicate sustainability information to investors.

The Carbon Disclosure Project (CDP

The Carbon Disclosure Project (CDP) is a nonprofit organization that uses software to help companies disclose on their environmental impact. Originally focusing only on climate change, the CDP has expanded to also include disclosure on water security and forests. The CDP interestingly borders between both a standard and a framework. It is more prescriptive in what needs to be disclosed than other frameworks and therefore in line with reporting to the GRI and SASB but contains items from frameworks such as the TCFD. Each year companies can fill out the CDP questionnaire which are freely available to view from their website. In addition, the CDP also scores each company’s submission on the level of detail and comprehensiveness provided in the response as well as the companies awareness on social issues, its management set up and progress towards environmental goals.

A Migrating Landscape

While each framework and standard have a different purpose and caters to a different audience, there is still a lot of overlap between them. Shareholders also saw this and have started pushing to consolidate the landscape and create some sort of consensus on sustainability reporting.

So, what is happening?

First, we have the International Financial Reporting Standards (IFRS), the organization responsible for developing a cohesive global accounting standard. This organization has also taken it upon themselves to develop a global baseline for corporate sustainability disclosure in what will be known as the International Sustainability Standards Board (ISSB). Do you remember SASB and IIRC merging in 2021 to create the Value Reporting Foundation? Well, as of June 2022 the Value Reporting Framework together with the CDSB will be merging into the IFRS to help develop the ISSB. Finally, the TCFD and GRI have entered into collaborative agreements with the ISSB to help draft the disclosure standards.

Next, we have the European Union who in their quest to become the first climate neutral continent by 2050 has developed the European Green Deal. Part of this deal includes the Corporate Sustainability Reporting Directive (CSRD). As stated by the European Union (2021), “the goal of the CSRD is to ensure that companies report reliable and comparable sustainability information needed by investors and other stakeholders. That would facilitate a consistent flow of sustainability information through the financial system.” Essentially, large companies will be required in 2024 to disclose sustainability information in the same rigor as with financial disclosures. The European Financial Reporting Advisory Group (EFRAG) has been tasked with developing the reporting standards. Again, the GRI and TCFD will be consulting with EFRAG during the development of the standards. Further both the IFRS and EFRAG have made bilateral agreements to consult each other in the development of the different standards.

Sources:

https://www.europarl.europa.eu/legislative-train/theme-a-european-green-deal/file-review-of-the-non-financial-reporting-directive#:~:text=Overall%2C%20the%20proposal%20aims%20to,information%20through%20the%20financial%20system.

creating momentum, delivering results.

- EMEA, +31657765304 I Americas, +1 7048072152

- office@sustainability360.ai

- www.sustainability360.ai

- All Rights Reserved © 2022

creating momentum, delivering results.

©2022 Sustainability360. All rights reserved.